By Donal Whelton

2020 to date has been somewhat surreal, with Covid-19 recreating the norm and, through interventions taken to curb its spread, supressing global demand and enforcing output price cuts across many sectors.

Thankfully, many commodity prices have rebounded somewhat as economies re-open, but with the incidence rate of Covid-19 again on the rise, how sustainable is the recovery and will it be sufficient to mitigate the challenges encountered? Only time and a bit of homework will tell.

It’s useful at this stage of the year to take stock, review and reflect on farm performance, and to put plans in place for the weeks and months ahead.

Dairy commodity prices dropped significantly following the closure of EU food service, however with economies re-opening and weather constrained supply across key exporting nations, prices and market sentiment have recovered, albeit the recovery has now started to plateau. All processors are now paying a milk price of 30 c/l including VAT or above, with the annual average milk price for the year as a whole likely to be at somewhat similar levels.

After recovering somewhat after initial declines, traditional increasing supplies is putting downward pressure on sheep and beef price presently, with the increased incidence of Covid-19 within meat processing plants particularly concerning.

After reaching record highs, pig prices have fallen 32c/kg since the onset of Covid-19, but have firmed up at €1.64 to €1.68 per kg in recent weeks. Market fundamentals remain strong, and favourable feed prices are helping preserve margin-over-feed somewhat.

Reports of both yield and quality across winter crops have been mixed to date. Drought impacted regions are harvesting as low as 2.5 tonne an acre; with less impacted regions returning three to four tonne per acre.

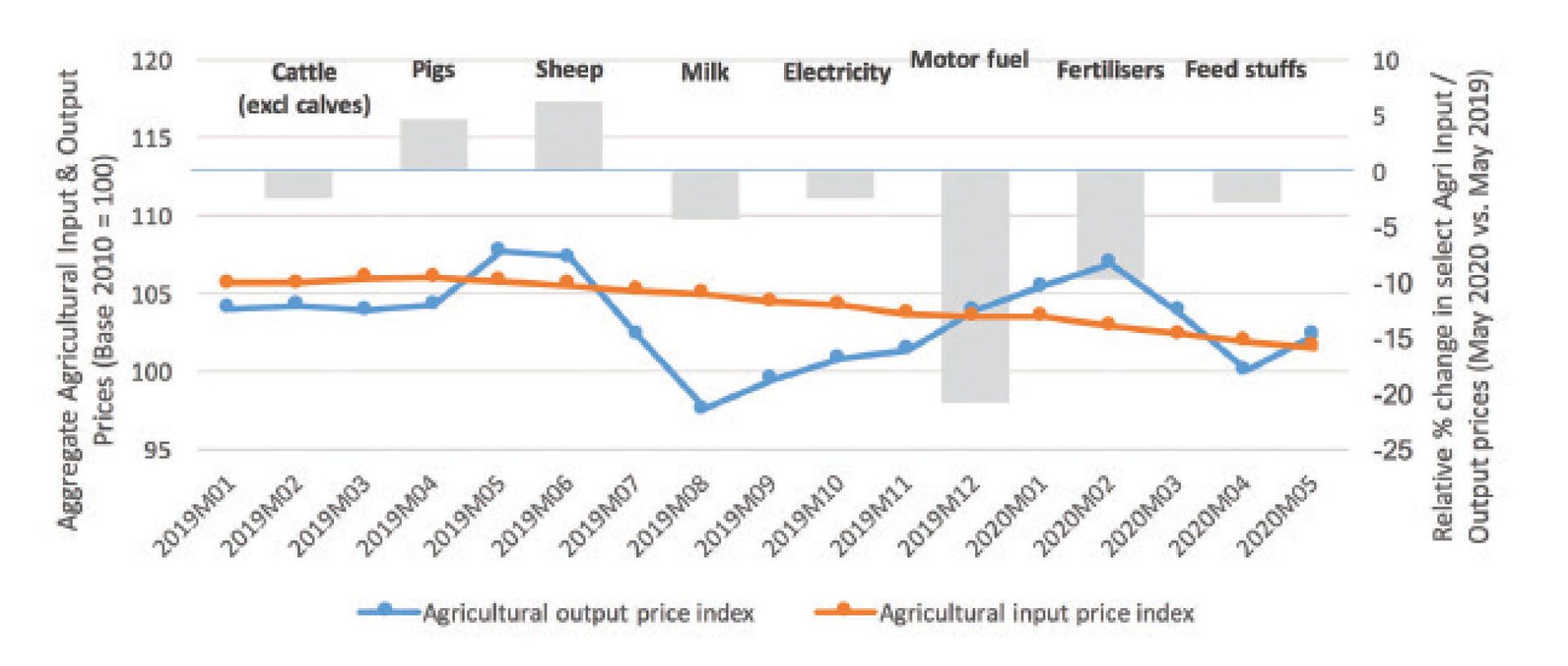

Across all sectors, reduced input prices (in particular, fuel -21%; fertiliser -10%; feed -3% May 2020 v May 2019) are helping mitigate, at least to some extent the decline in output prices, and preserve margins. Recent CSO data for May 2020 suggests, overall, a 1% reduction in terms of trade, with aggregate output prices declining 5.4% and aggregate input prices declining 4.3% year-on-year.

Looking ahead, whatever outcome Brexit brings remains the big uncertainty, and indeed challenge for the sector. There also of course exists the possibility that, similar to other economies, a second wave of COVID-19 appears, forcing a reintroduction of restrictive measures to curb its spread. The hope remains that the country will not revert into the severe lockdown state that phase one brought.

To find out more how AIB can support you and your business into the future contact your AIB relationship manager, call 1890 47 88 33 (available 9am to 5pm on weekdays) or visit www.aib.ie/farming.

Lending criteria, terms and conditions apply. Credit facilities are subject to repayment capacity and financial status and are not available to persons under 18 years of age. Security may be required.

• Donal Whelton is a senior agri advisor at AIB.